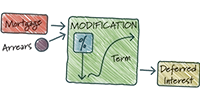

The most effective strategy our firm employs to prevent foreclosure for homeowners in significant mortgage arrears is mortgage modification. Many homeowners facing foreclosure are seeking retention options—solutions that enable them to resolve mortgage issues while keeping their homes.

Through mortgage modification, overdue payments are integrated into the remaining principal balance, reducing the immediate foreclosure risk. The objective is to establish affordable monthly payments, even if the total loan amount increases. This can be achieved by:

A successful mortgage modification should achieve two main goals:

Our team is dedicated to helping homeowners find practical and effective mortgage solutions to safeguard their homes from foreclosure.

Currently, mortgage loan modification is the most popular and effective solution for homeowners looking to resolve mortgage arrears, stop foreclosure proceedings, and retain their homes. However, if a mortgage modification is not feasible or preferred by the borrower, other retention options are available for properties in default.

In cases where no retention options are suitable, we also offer guidance on non-retention alternatives, which are for homeowners who choose not to keep their distressed properties. These options are detailed in our “Debt Negotiations and Settlements” section.

With our law firm’s extensive experience in mortgage loan modifications, our skilled team can significantly improve your chances of securing approval. If a modification is not viable, we will thoroughly evaluate and explore other retention strategies to find the most effective solution for your situation.

Negotiating mortgage modifications can be complex and time-consuming, but they remain one of the most effective ways for homeowners to make their mortgage payments more affordable.

In today’s economic climate, many homeowners face financial hardships due to mortgage arrears, making modification agreements a crucial solution. However, to qualify, a borrower must demonstrate both financial hardship and stability to ensure they can sustain payments under the new terms.

Several key factors influence a homeowner’s eligibility for mortgage modification, including:

By carefully evaluating these factors, our experienced legal team guides clients through the modification process, increasing their chances of approval and long-term mortgage affordability.

Since the 2008–2014 recession, triggered by overly aggressive mortgage lending and borrowing, mortgage modifications have become increasingly sought after and more accessible. Many foreclosures and unresolved mortgage issues are lingering effects of the previous recession, which continue to impact homeowners today. Despite significant improvements in the economy since then, the COVID-19 lockdowns, furloughs, and layoffs caused a major setback. As a result, many homeowners have fallen behind on their mortgages, with many already facing foreclosure or at risk of it. Although this crisis has left homeowners in financial distress, it has also put pressure on mortgage lenders, as well as federal and state governments, to find better solutions. Seeking a mortgage modification or another negotiated resolution with one’s lender plays a critical role in addressing this issue.

In February 2009, the federal government launched a voluntary initiative aimed at encouraging mortgage lenders to modify loans for “at-risk homeowners” through legislation enacted at that time. Homeowners could apply to their mortgage lender for a modification under the Home Affordable Modification Program (HAMP). However, lenders were not required to reduce the loan principal; instead, they could lower the monthly payment by extending the loan term or reducing the interest rate.

An aspect of the original legislative proposals, which was rejected by the Senate, would have granted bankruptcy judges the power to mandate mortgage modifications if a lender rejected legitimate requests. Currently, mortgage lenders have the right to reject or ignore loan modification requests, as these modifications are voluntary.

To qualify under HAMP, homeowners needed to be deemed “at risk” due to significant hardships, such as income loss, increased expenses, or “payment shock” (resulting from much higher mortgage payments). By June 2012, the basic requirements for HAMP were revised for many loans, allowing second mortgages and equity loans without disqualifying borrowers. Homeowners also had to be in default or at risk of default.

Borrowers had to meet the eligibility requirements, even if they were not behind on payments, as long as they had enough income to meet the adjusted payments. Lenders could reduce interest rates to as low as 2% and, if necessary, extend the loan term up to 40 years to reduce mortgage payments exceeding 31% of gross income. In exchange for offering these loan modifications, the federal government provided financial incentives to mortgage servicers.

Although the HAMP program ended on December 31, 2016, it encouraged lenders to create their own, more flexible “in-house” modification programs. Under both HAMP and these “in-house” programs, mortgage arrears and the remaining principal balance would be combined, the interest rate lowered, and the loan term extended, resulting in a larger loan with lower monthly payments. After HAMP’s conclusion, the focus shifted to private non-HAMP modifications, now available from nearly all major lenders. Borrowers no longer need to undergo an initial screening for HAMP; an in-house modification is only considered if the borrower is ineligible for HAMP.

While HAMP began with modest loan rates of 2-3%, these rates gradually increased. Despite the advantages of financial subsidies and government monitoring, HAMP became burdened by additional rules, paperwork, and administrative layers. In many ways, current non-HAMP, private “in-house” modifications are faster and simpler, but they lack the federal oversight that HAMP provided. However, after HAMP ended in 2016, the number of Chapter 13 and 11 bankruptcy cases rose, with “loss mitigation” plans becoming a central part of reorganizations. These bankruptcy cases, focused on “loss mitigation,” offered judicial oversight of the modification process.

The economic effects of the Covid-19 pandemic are expected to cause many more homeowners to fall behind on their mortgages. To address a potential new foreclosure crisis, new government and private initiatives may be necessary, offering innovative solutions.

Many homeowners in Brooklyn’s Suffolk and Nassau Counties who are struggling with mortgage payments seek help from mortgage modification attorneys like the Law Office of Ronald D. Weiss, P.C. The process of applying for a mortgage modification or other retention options can be complex, making professional representation crucial. While negotiating mortgage modifications and retention options can be beneficial, it is often difficult and unpredictable, as many mortgage holders and their attorneys resist negotiated offers. This requires a strategic and persistent effort.

Our firm takes a comprehensive approach to mortgage and foreclosure solutions, ensuring we explore multiple options to resolve mortgage issues. While mortgage modifications are a priority, we do not rely on them exclusively. Securing better mortgage terms and resolving mortgage problems is our goal, even though the process can be time-consuming and complicated. Here’s why you should consider our office to represent you:

If you’re struggling with your mortgage, the Law Office of Ronald D. Weiss, P.C. can help you pursue a mortgage modification or other retention options. For more detailed information on Mortgage Modifications, click here.

To ensure the success of modifications or retention options, hiring a qualified professional is essential. We advocate on your behalf using applications, letters, calls, and supporting documents to persuade your lender to modify your mortgage.

The Law Firm of Ronald D. Weiss, P.C. has successfully facilitated thousands of agreements, assisting clients in resolving mortgage arrears. Thanks to our efforts, many homeowners have avoided foreclosure and been able to retain their homes through various agreements, including mortgage modifications, forbearance agreements, payment plans, short sales, deed-in-lieu agreements, and other settlements. By choosing us to represent you, we ensure that the foreclosure process is managed efficiently, with timely resolutions. We also ensure that settlement terms are documented in a legally enforceable written agreement to safeguard your rights.

Our consultations are free, and the advice we provide could be invaluable.

To discuss these negotiation and adjustment options in more detail, please contact us at (631) 250-4120 or email weiss@ny-bankruptcy.com for a complimentary consultation.